Buying your first home is an exciting milestone in your life, but it can also be overwhelming. If you’re unsure what steps to take when finding and applying for a mortgage, we’ve provided this guide to get you through the basics every step of the way, from sketching a budget to signing on the dotted line.

Want to talk through your mortgage options with an expert? Reach out to us today.

Understanding the Basics

Let’s start off by defining some important mortgage terms that you will hear often:

- Principal: The amount you borrow for your home loan.

- Interest Rate: The percentage of the principal amount you pay to your lender. Interest is a fee your lender charges for lending you money.

- Annual Percentage Rate (APR): The true cost of your loan, including interest and fees.

- Amortization: The way you pay your principal and interest off over time. For more information about Amortization, refer to this article.

- Private Mortgage Insurance: Protects your lender if you default on your home. Required if you put down less than 20% of your loan’s principal amount.

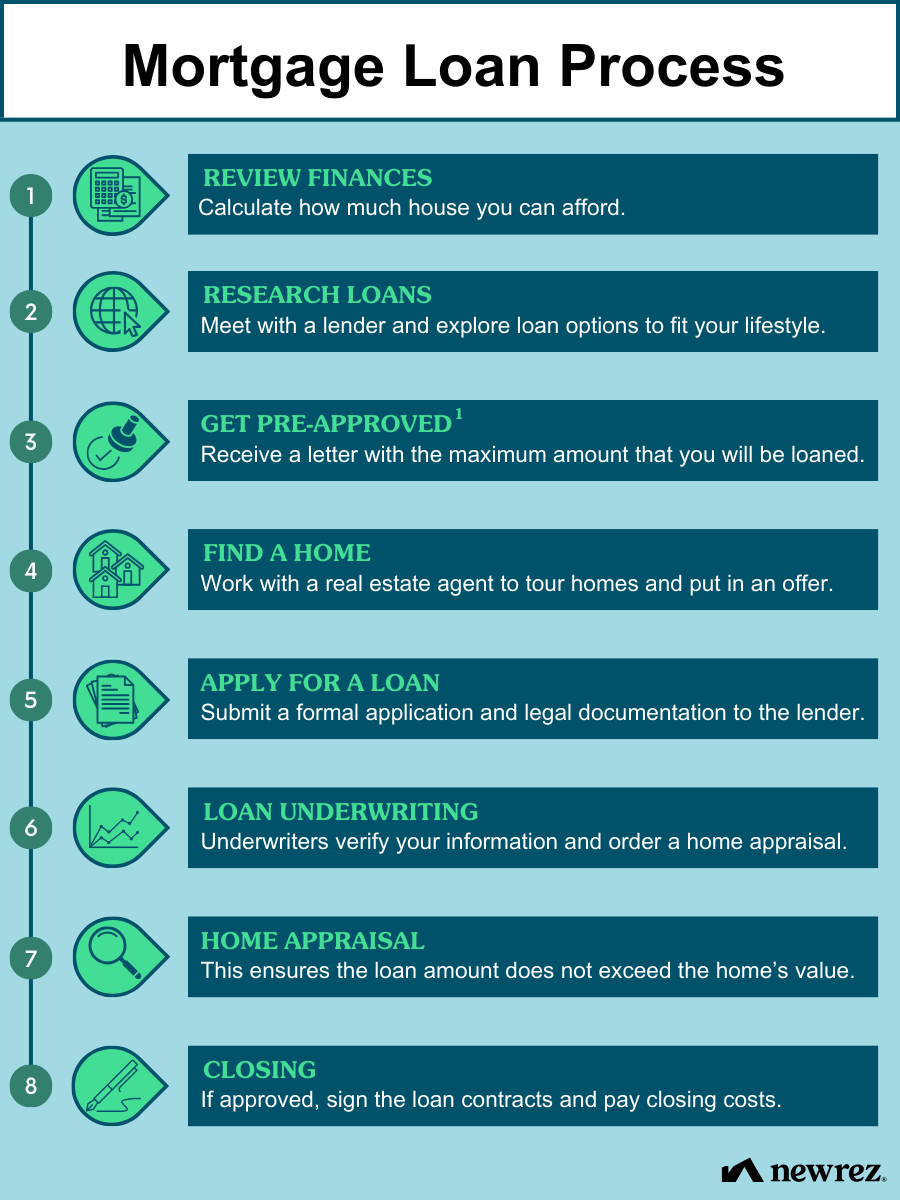

The graphic below provides a quick overview of the whole mortgage loan process, and then we’ll get into the details:

Preparing Financially Before Applying

A mortgage is a major long-term investment, and you want to be sure you can handle both the upfront costs and a monthly mortgage payment. Keep in mind that your lender will be assessing your finances to see what size loan you may qualify for.

- Set a Budget: Look at your monthly income and expenses and get a rough idea of how much monthly mortgage payment you can accommodate. Use our Home Affordability Calculator to calculate how much house you can afford.

- Get Pre-Qualified2: Call up a lender and provide self-reported financial information so the lender can give you an estimate of what loan you might qualify for. (Learn about the difference between pre-qualification and pre-approval.)

- Gather Necessary Documents: Track down recent pay stubs, bank statements and other documents needed to verify your income and assets to a lender during pre-approval.

- Prepare for the Down Payment and Upfront Costs: Look at your assets and determine how much you want to put down on a new home. (You don’t always have to put 20% down.) Then plan for closing costs like appraisal fees, loan origination fees and beyond.

- Avoid Making Major Financial Changes: It’s in your best interest to not make major purchases or switch jobs just before applying for a mortgage. Lenders want to see stability in both your income and your credit.

Evaluating Mortgage Options

Different mortgages offer a variety of loan conditions to suit your financial goals and lifestyle. If you like, you can talk with a Newrez loan expert about your particular circumstances, and they can help you find a great loan. Here are just a few options:

Conventional Loans

- Usually require a strong credit score, but may allow for flexible term lengths.

Federal Housing Administration (FHA) Loans

- Often carry lower credit score requirements than conventional loans, as well as flexible debt-to-income (DTI) ratio requirements.

- May enable you to qualify with as little as 3.5% down. Learn more.

Veterans Affairs (VA) Loans

- Available to eligible Veterans, active-duty service members and surviving spouses.

- May allow eligible borrowers to qualify with no down payment. Learn more.

U.S. Department of Agriculture (USDA) Loans

- Created for borrowers with low-to-moderate incomes living in rural or suburban areas.

- May allow borrowers to put no money down.

Non-Qualified Mortgages (Non-QM)

- Available for self-employed borrowers, investors, high-net-worth individuals and beyond. Learn more.

Renovation Loans

- May enable you to fund renovations for a fixer-upper home within a single mortgage payment. Learn more.

Getting Pre-Approved1

Getting pre-approved is a good idea for a couple of reasons: Firstly, it’ll give you a clear idea of what you can afford. Second, it’ll strengthen your offer to a seller.

- Define Clear Budgetary Limits. Getting pre-approved can help focus your search on homes within your means.

- Demonstrate Your Buying Power. Show the seller you have the finances to back up your offer and you’re a serious buyer.

- Receive Conditional Approval. In order to get pre-approved, a lender will do an in-depth analysis of your financial situation, including your income, assets and credit. Pre-approval represents conditional loan approval by a lender, meaning you are approved subject to certain conditions being met later in the home buying process, such as the execution of a purchase and acceptable appraisal and title documentation.

Completing the Mortgage Application

So you’re ready to commit to a home – congratulations! Now is the time to finish your mortgage application. You may have already completed much of the application process during pre-approval, but the full mortgage application requires just a few more items, including but not limited to:

- Purchase agreement

- Proof of your earnest money deposit

- Any updated info about your income/assets

At this point, you will typically receive a loan estimate that details rates, fees and terms.

Mortgage Processing and Underwriting

Once you’ve submitted your application, it will undergo these steps:

- Processing: The lender will verify the accuracy of the information you’ve provided and will review credit information, titles and tax transcripts. Any discrepancies will need to be explained in writing.

- Underwriting: An underwriter will review the information with a fine-toothed comb and evaluate how much risk the lender is taking on. They want to be sure you have the capacity to make your payments, that you’re likely to make them on time and that the loan aligns with the home’s value. You may be required to answer more questions.

Finalizing the Closing Process

The countdown to moving into your new home involves a lot of fees and forms, so be sure to prepare accordingly and keep track of everything.

- Do a final walkthrough to be sure the property is in the agreed-upon condition.

- Your lender will usually send closing documents and instructions to your attorney or title company. Your signature will be required on many documents.

- The Closing Disclosure confirms final fees and loan terms.

- Pay closing costs and any remaining down payment.

At this point, the lender releases the funds, the transaction is recorded with local authorities, and you get your keys!

Your Responsibilities as a Homeowner

Achieving homeownership is cause for celebration, but it’s also just the start of your homeownership responsibilities. Be sure to stay on top of your finances so you’re always able to make your monthly mortgage payment, and you’re able to handle repair costs as they arise.

Curious to know what all is included in your mortgage payment? Read this article.

Looking for a mortgage company that will help you find the right loan for you? Chat with a Newrez mortgage expert.

1 A pre-approval does not signify that all underwriting requirements have been met. Actual terms, including interest rate, are subject to change without prior notice and may vary based on eligibility criteria. All products are subject to credit and property approval. Not all products are available in all states or for all dollar amounts. Other restrictions and limitations apply.

2 Offer is contingent upon a full credit review. A pre-qualification does not signify that all underwriting requirements have been met. Actual terms, including interest rate, are subject to change without prior notice and may vary based on eligibility criteria. All products are subject to credit and property approval. Not all products are available in all states or for all dollar amounts. Other restrictions and limitations apply.

National Association of Realtors® is a registered trademark of the National Association of Realtors and is not affiliated with Newrez LLC.

Reference:

2024-profile-of-home-buyers-and-sellers-highlights-11-04-2024_2.pdf